Yep...I'm back!

After another hiatus, here I am. Now I'm not satisfied with just posting, I want to be in your mail box.

It’s been a while, I know. But I also know nobody really misses my write-ups. So, I guess what I’m trying to say is: sorry for disturbing the peaceful silence of your inbox after so many months.

The last time I wrote about my portfolio was in a post at the beginning of the year. Looking back, I think I misrepresented it a bit. I have an FGTS fund that invests in Eletrobras, which I didn’t mention, and I also skipped my cash position. I didn’t make a huge mistake — the cash portion wasn’t big — but the Eletrobras fund was probably more relevant then than it is today.

A lot of people have a lot to say about the Brazilian stock market.

I don’t. Whatever I say wouldn’t express my opinion better than my portfolio does today.

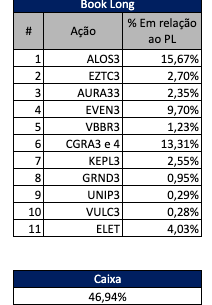

As you can see, I currently have four convictions, and cash is the strongest of them. It’s an asset backed by the government, denominated in its own currency, yielding around 15% per year, with no price risk. I don’t know — that just seems good enough to me.

Call me a rentista. I don’t care.

The rest of my convictions are valuation- and yield-based. As I said in that earlier post, considering where interest rates are today, I need to see cash being generated. And the best way for a company to show me that is by actually giving me the cash.

But dividends alone are never enough. I also need to believe that the cash-generation machine is sustainable — and growing, if possible. That’s where things get difficult. You really have to carve out time and do the work to understand a business’s earning power, or at least estimate its asset value on a reproduction-cost basis. And finding that time seems to get harder every year.

Since I don’t have enough conviction in my new ideas, I’ve had to make them smaller than I’d like. That’s where I am with KEPL, GRND, UNIP, and VULC — all new positions, though UNIP and VULC have appeared in my portfolio once or twice before. VULC, in fact, predates this blog, and is now a much better company.

EZTC is a bit of a different case. My idea was to reduce my position in EVEN, replacing it with a company in the same sector - one with better earnings-power prospects at a cheap enough price. That was the context when I came across EZTC in the mid-July. But as soon as I dipped my toes in, the stock jumped about 15%, and then I started wondering whether the other candidates might be a better fit.

VBBR and AURA are positions in transition. I’m still selling AURA — and what a ride that’s been. One of the most beautiful cases I’ve ever invested in. But now, I just don’t see enough margin of safety to stay in, so I’m getting out, little by little. Most of my AURA turned into cash this year. (My last post about the company was this one.)

VBBR, on the other hand, is not at a price that makes me want to sell. I will wait fot the market to offer a better one - or sell, if another more compelling opportunity appears.

In my first post of the year, I listed a few companies that I thought fit the environment as I saw it: UNIP, VULC, and KEPL were on that list; GRND was the only one missing. Now my challenge is deciding whether to increase allocation in any of them. I also have one more name on my watchlist — CAMB. Although it’s harder to picture growth in the coming years, there may be other opportunities there that aren’t yet visible on the surface.

Since I’m struggling to establish the earning-power of the companies that interest me, maybe I should be buying long-duration government bonds instead — the NTN-Bs 10-years-plus. I’d benefit if rates fall and avoid company-specific risk. What’s kept me in LFTs so far has been interest-rate risk: I had the feeling rates could rise further, and if I found a market opportunity, I’d need to sell at a loss. But if I size this position like I would a stock, maybe I can have my cake and eat it too.

What else?

Other things I want to look into:

Possible problems with my portfolio

Master Bank

Ambipar

Reag

Cosan

Braskem

Dividends vs. Growth

Accounting peculiarities, fraud, and short selling

Economic and investment cycles

Which one should I dive into next? Drop your pick in the comments!

Cheers, and see you soon!

PS: You can read this post in Portuguese on the Substack page [here].

8. 😀

Venha para o renda ÷ 65!!! Bora ser rentista!!!